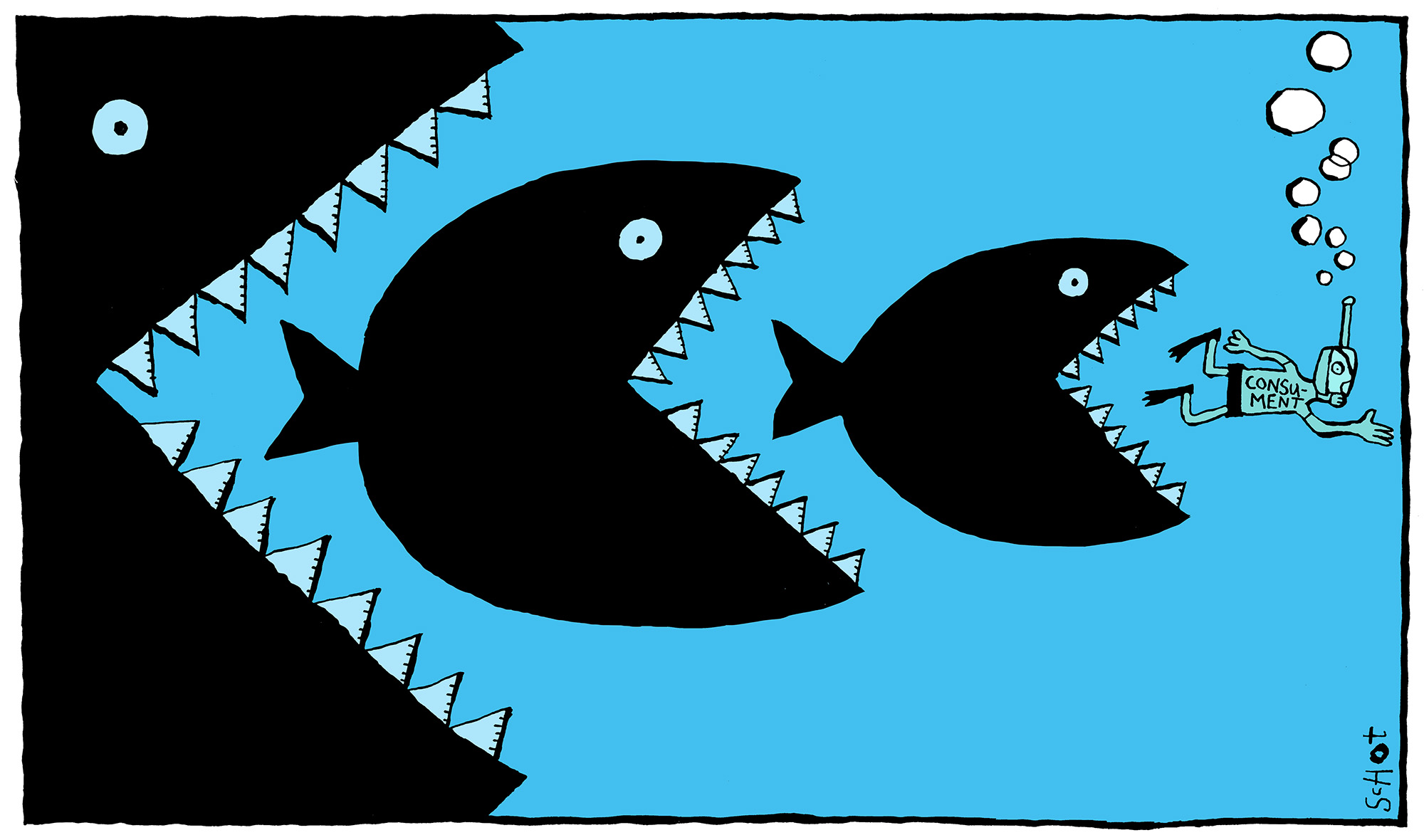

‘It is unfair that economists should be given such a dressing-down’

Image by: Bas van der Schot

Een lijst met artikelen

-

How the free market destroyed a successful Dutch company

Gepubliceerd op:-

The Issue

-

Shareholders are overly focused on the short term, Professor of Sociology Johan Heilbron said while discussing his book, entitled De Zaak Organon [The Organon Case]. How do you feel about this?

“It is simply incorrect. Let me give you an example: Tesla. There is no evidence that that company will live up to Elon Musk’s expectations, but it does have a market value of 51 billion dollars. This is purely because the shareholders are willing to invest in the future along with the CEO. I have no doubt there are shareholders who focus more on short-term interests than on long-term interests, but that, too, serves an important purpose. The share market works by the grace of supply and demand. People sell their shares or options when they first find themselves thinking, this is heading in the wrong direction. These signals are indispensable to a properly functioning market. We must avoid getting ourselves into a situation where managers whose companies are performing poorly can hide behind the excuse of focusing on the long term.”

Organon, which used to be part of AkzoNobel, was sold, resold and dismantled within the course of just a few years, thus decimating one of the most important pharmaceutical companies in the Netherlands. The authors of the book sketch a course of events in which an underperforming American company called Schering-Plough acquired Organon in an attempt to deflect attention from the claims and fines with which it was about to be hit. Dressing up the bride, Heilbron called it. Wasn’t that rather a clear example of the market not functioning properly at all?

“This is one example where I can’t tell whether people were trying to pull a scam or not. But as far as I’m concerned, [the authors] leaped to a conclusion on Schering-Plough’s motives. Of course the demise of Organon is regrettable, but then it had been up for sale for ten years. Sure, for Hans Wijers (the CEO of AkzoNobel at the time – ed.) to decide within one day to sell the company, and for shareholders to have to witness that sale being pushed through even though the board of supervisors was against it… as far as I’m concerned, that is the crux of the problem. The way things are now, people are giving too much of the blame to the buyer and the shareholders.”

‘I do somewhat object to people saying that the Dutch crown jewels were being frittered away’

The sale of Organon was not given much attention at the time. More recent attempts at takeovers, e.g. last year’s attempted takeovers of AkzoNobel and Unilever, attracted a great deal of sudden action to prevent these Dutch crown jewels from falling into foreign hands. Do you think this is a good thing?

“I think it’s a good thing that there was a public debate. I do somewhat object to people saying that the Dutch crown jewels were being frittered away. The Akzo takeover was initiated by PPG, a buyer who had highly valid reasons to look into the company’s current share price. But the media completely focused on the motives of another buyer, activist shareholder Elliot. What is much more important is the question as to whether Dutch companies are sufficiently well equipped to withstand the challenges with which our changing world will present them. And as far as that is concerned, I think Heilbron was very quick to criticise economists and – indirectly – analysts.”

Heilbron does indeed accuse economists of only taking into account figures, cash flows and other quantitative variables they can incorporate into their models when assessing companies.

“I disagree with that. Analysts also consider aspects relating to management and aspects relating to culture. Of course they use models in doing so, but what’s wrong with that?”

We need different and stricter regulation, Heilbron says. Do you agree with that?

“Additional protection from takeovers is unnecessary, the only exceptions being companies in the infrastructure industry, such as Schiphol Airport, the Port of Rotterdam and power grid operators. They are too vulnerable to be allowed to fall into foreign hands. However, companies should pay greater attention in their financial reporting to issues their businesses will have to tackle in the long term – climate change, artificial intelligence, that sort of thing. For instance, lithium is one of the key fuels for electric cars. Manufacturers will become dependent on it, which will greatly affect the price of lithium. Management teams should include that kind of information in their reports.”

Paul Koster is the Chairman of the Vereniging van Effectenbezitters (VEB, ‘Association of Shareholders’), which has promoted the interests of Dutch investors since 1924. By its own account, VEB has 42,000 members, including both private investors and institutional investors such as pension funds and insurance companies.

De redactie

Latest news

-

Community service and suspended prison sentence for founder extreme-right student party

Gepubliceerd op:-

At the neighbours

-

In court

-

-

ESL PhD candidate loses lawsuit over Gaza letter

Gepubliceerd op:-

In court

-

-

Europe wants to double science budget and distribute it more fairly

Gepubliceerd op:-

Science

-

Comments

Comments are closed.

Read more in The Issue

-

‘Most medical influencers do not think they are unqualified’

Gepubliceerd op:-

The Issue

-

-

War in Iran: will the energy transition get a push or a blow?

Gepubliceerd op:-

The Issue

-

-

How expensive festival tickets and major concerts are threatening the entire live music sector

Gepubliceerd op:-

The Issue

-