How the free market destroyed a successful Dutch company

According to the authors of De Zaak Organon, which provides a reconstruction of the dismantling of a once highly successful Brabant-based pharmaceutical company called Organon, companies’ obsession with shareholder value is proving disastrous to the investment climate and innovation. Sociologist Johan Heilbron: “We need better regulation, and soon.”

Johan Heilbron is a Professor of Sociology at Erasmus University. He specialises in economic sociology, among other things. In association with Jack Burgers, a Professor of Urban Studies, he wrote the book De Zaak Organon (Prometheus, 2018). In addition, he is affiliated with the Centre Européen de Sociologie et de Science Politique (CESSP) in Paris. He is currently working on a book on the globalisation of social sciences at Princeton University’s renowned Institute for Advanced Study.

What prompted two sociologists to write a book on a corporate takeover?

“For my colleague Jack Burgers, it all started in his place of residence, Oss, with stories of employees who might be about to lose their jobs. His general practitioner told him about the large number of people who were suffering from the great uncertainty caused by the looming dismissals. My own interest was piqued by the question as to why the once highly regarded Organon laboratories were closed. Were they no longer competitive or was there much more to the story?

“By mapping out the growth of the company since its foundation in 1923, we are revealing some of the dynamic that can be seen in other companies as well. Moreover, in association with our master students, we examined the social and economic consequences of the company’s closure. And even though the book is about Organon and Oss, such takeovers, closures of companies and questions as to whether the government should intervene in a globalised knowledge economy are the order of the day.”

Within the course of a few years, Organon, which used to be part of AkzoNobel, was sold, resold and dismantled. As a result, one of the key pharmaceutical companies of the Netherlands was decimated. What happened?

“We like to call it playing poker with companies. The sale and resale was a stock market game in which the company itself – including its products, knowledge and employees – was considered of secondary importance. Organon’s buyer, Schering-Plough, had been in trouble for several years. When it made an offer on Organon in 2007, it was facing a huge scandal. In order to get its money before the bad news broke, Schering-Plough purchased Organon, and soon afterwards organised a major press conference, at which it made much of the new medications it was going to market, partially thanks to Organon. This is called ‘dressing up the bride’.

“That prospect was tantalising enough for the even larger pharmaceutical company of Merck to make an offer on Schering-Plough. This takeover, which ended up costing sixteen thousand jobs, helped Schering-Plough’s CEO, Fred Hassan, earn a whopping 189 million dollars. When the expanded Merck was restructured, it was found that it could only accommodate the most lucrative products and the most promising patents. As a result, Organon’s research departments were closed.”

Image by: Bas van der Schot

‘The core of the problem is the fact that shareholders, private equity and hedge funds are now in charge’

Organon was supposed to go public. Why did this not happen?

“Because AkzoNobel’s board, led by Hans Wijers, accepted the offer made by the American pharmaceutical company of Schering-Plough two weeks before the scheduled initial public offering. Hans Wijers told us in an interview that this decision was made on the same day the offer was made. Wijers also stated that Schering-Plough would provide a good ‘home’ to Organon. This is extremely curious, because the members of AkzoNobel’s supervisory board who were tasked with the pharmaceutical side of the business were firmly opposed to the takeover and resigned because of it.

“So if Wijers knew what kind of company Schering-Plough was, he did not tell the truth. And if he did not know, he acted in an irresponsible manner by selling Organon in one day. Neither case is remotely in compliance with the Dutch Corporate Governance Code, which clearly does not work well in these sorts of cases.”

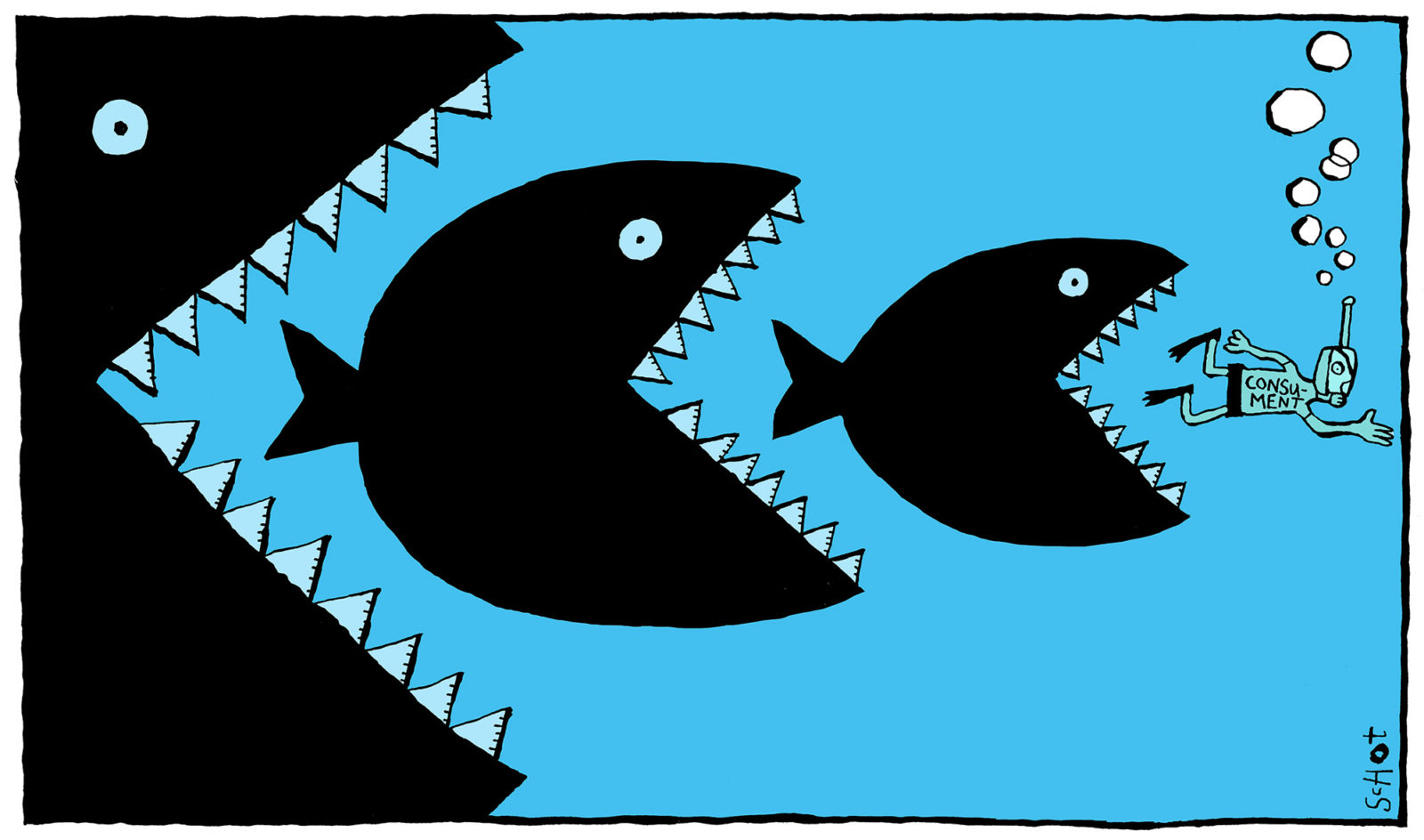

International investors also wrought great havoc on V&D and the selexyz chain of bookshops. What is going wrong here?

“The core of the problem is the fact that shareholders, private equity and hedge funds are now in charge. They make highly profitable deals, but give no thought whatsoever to the long-term interests of the companies they buy. To give you an example: research conducted in the United States shows that on average, investors only hold shares for half a year. After that they are resold to a third party.”

Image by: Bas van der Schot

Isn’t there a positive side to all of this in that the resulting companies operate in an efficient and innovative manner?

“Quite the contrary. Their obsession with shareholder value has resulted in decreasing investments, reduced innovation and greater payments to shareholders (in the form of dividend and the company’s purchase of its own shares). Genuinely innovative and risky research is increasingly being outsourced, and is now carried out by small start-ups and government-owned laboratories. For this reason, American prizes for innovative products have increasingly not been awarded to corporate labs in the last thirty years.

“Just think it over – a high-tech company such as Organon depends on research whose products can only become commercially interesting in the long term. This means that such a company must be run on the basis of a time horizon of at least ten years. In other words, such businesses need patient capital, but they are not or hardly getting any.”

What kind of damage did the squandering of Organon cause?

“It is a huge problem that knowledge-intensive and complex businesses are subjected to short-range financial transactions in this manner. In the Netherlands, some two thousand jobs were lost when Organon folded. Five hundred jobs were regained when former employees established companies of their own with others. That is quite the loss. But globally, some twenty thousand people worked at Organon, a great many of whom also lost their jobs. And a great many other things were lost as well, in addition to jobs: knowledge, experience, economic diversity in the region. Such closures have consequences whose effects can be felt for years in a wide range of respects. For instance, highly lucrative medications were born of the Organon estate – medications in which Schering-Plough and Merck were not the slightest bit interested. Creative destruction, economists call this, referring to the process of continuous innovation in which old companies and ideas are replaced by new ones. Well, this particular destruction was very far from being creative.”

‘Academic economics is part of the problem’

Last year both Unilever and – how very ironic – AkzoNobel were protected from hostile takeovers. Has the Netherlands finally realised the danger inherent in such takeovers?

“The market for corporate takeovers, be they voluntary or involuntary, works poorly. This has been known for quite a while now. Many takeovers and mergers are unsuccessful, and they often result in the acquired businesses being dismantled. It is high time that parties not being activist shareholders – i.e. entrepreneurs, employees and long-term shareholders – looked into this and protected themselves from such practices.

“In addition, we urgently need improved regulation of the market. I think one of the best measures would be to restrict shareholders’ voting rights in strategic decisions to people who have held their shares for at least one year. Or, alternatively, we could institute a right of withdrawal in the event of a takeover, as Jan Hommen (CEO of KPMG and former general manager of ING – ed.) has proposed. We could even consider certain protective constructions, although these should obviously not be used to protect failing managers. What with all the takeover horror stories of the last few years, I think a comparative study of regulation regimes would be extremely useful.”

Both you and your fellow author are sociologists. Don’t you think this book should have been written by an economist or business administrator?

“Academic economics is part of the problem. Every year, thousands of economists and business administrators graduate from university, but strangely enough, no one has ever written a thesis on the Organon affair. There are several reasons for this.

“Economists assume that there is a market for corporate takeovers, and that this market operates in the way markets are presumed to operate. That is the matter with market fundamentalism: the unshakable belief that the outcomes of market transactions are efficient.

“In addition, economists tend to be more interested in models than in economic reality. They seldom conduct archival research, interviews or observations of economic transactions. If you don’t feel like doing these things, fine, but then at least collaborate with historians or sociologists! They don’t do that either. Out of all social scientists, economists are the least likely to collaborate with researchers representing other disciplines.”

That is quite the dressing-down. What is it sociologists do better than economists?

“Sociologists don’t regard businesses as monolithic ‘agents’ that maximise their usefulness or their shareholders’ usefulness. Rather they regard them as combinations of departments and groups with differing opinions on the company’s duties. In the Organon case, they had differing opinions on the balance of power between the research departments and the department responsible for marketing and sales. The fact that the research departments had held a relatively strong position ever since the foundation of the company is one of the main reasons why Organon was so successful.

“But this internal balance of power in turn depends on the changing ways in which businesses are embedded in the context in which they operate. This is a complex issue that cannot be captured in a basic formula. For instance, the sale of Organon cannot be understood without some understanding of the context of increased power for financial markets and shareholders, a widespread belief in efficient markets, and poor regulation of said markets. Economists tend to pay little attention to the context of economic behaviour and have actually contributed to the liberalisation of the financial markets and people’s tremendous faith in the market.”

De redactie

Latest news

-

Community service and suspended prison sentence for founder extreme-right student party

Gepubliceerd op:-

At the neighbours

-

In court

-

-

ESL PhD candidate loses lawsuit over Gaza letter

Gepubliceerd op:-

In court

-

-

Europe wants to double science budget and distribute it more fairly

Gepubliceerd op:-

Science

-

Comments

Comments are closed.

Read more in The Issue

-

‘Most medical influencers do not think they are unqualified’

Gepubliceerd op:-

The Issue

-

-

War in Iran: will the energy transition get a push or a blow?

Gepubliceerd op:-

The Issue

-

-

How expensive festival tickets and major concerts are threatening the entire live music sector

Gepubliceerd op:-

The Issue

-