How improving Dutch business climate dictates everything

Image by: Bas van der Schot

Even though there is no political support for the measure, the withholding tax on dividends in the Netherlands will in all likelihood be abolished. What is the return for the Netherlands from abolishing the dividend withholding tax, which costs 2 billion euros tax in revenue? Economist Bas Jacobs: “Our politicians are struggling to find a good economic justification, but there simply isn’t one.”

Bas Jacobs is professor of Economics and Public Finance at Erasmus School of Economics. He specialises in optimal taxation, macroeconomics and welfare economics. During this academic year he is Wim Duisenberg Fellow at the Netherlands Institute for Advanced Study.

Let’s start with the most important question: is there economic evidence that abolishing the dividend withholding tax will result in larger investment and more jobs?

“No. The economic reasoning of the government is shaky. That’s in part due to a lack of understanding of the nature of the tax. The dividend tax is generally withholding tax, similar to the withholding payroll taxes of employers. The tax is withheld from the dividends that companies pay out to their shareholders and it is then transferred to the tax authorities. In the vast majority of OESO countries, shareholders of companies who have paid dividend taxes in the Netherlands can subsequently credit their tax payments in the Netherlands against their personal income tax to avoid being taxed twice.

“This is important, because it undermines the reasoning that it will be easier to raise equity capital if there would be no dividend tax. Whether the dividend tax is abolished or not, it will probably have little effects on the willingness to invest or to create employment because it will have negligible effects on the user cost of capital for companies.”

Why is there such vigorous lobbying by companies such as Philips, Akzo Nobel, Shell and the employers’ organisation Confederation of Netherlands Industry and Employers VNO-NCW?

“As I understand it, multinational companies like Shell and Unilever, that have their headquarters located in both the United Kingdom and the Netherlands, have been badgered for many years by British shareholders who want to get rid of being taxed twice. This is because the United Kingdom is one of the few countries where shareholders can’t credit the dividend withholding tax they’ve paid abroad against their personal income tax. As a result, Unilever’s CEO Paul Polman now seems to be acting as a main representative of the British shareholders. That is very peculiar to say the least. The Dutch dividend tax is of course a nuisance to British shareholders, but I don’t see why it would create problems for Unilever. They can always find shareholders who don’t pay any dividend tax, such as our pension funds, or shareholders who can credit their withholding taxes against their income tax.”

Image by: Bas van der Schot

‘Due to these kind of things, people lose their trust in politics’

Almost 80 percent of the Dutch public is now against this measure. Yet it will still be implemented. How is that possible?

“It’s cynical. There is virtually no democratic legitimacy for the measure: no party had proposed it in their party manifestos during the last elections, ChristenUnie and D66 obviously oppose the measure. A majority of the Lower House doesn’t want it. However, it is politically fascinating that Mark Rutte introduced the measure during the coalition talks to form a new government, which took everyone by surprise. According to Gert-Jan Seegers (ChristenUnie), this was apparently a deal breaker. And now Rutte refuses to make a political turn to preserve his political credibility, even though he might have been conned by his corporate friends and the measure is not in the general interest. Due to these kind of things, people lose their trust in politics.”

Een lijst met artikelen

-

Controversial RSM study used as grounds for abolishing dividend tax

Gepubliceerd op:-

Campus

-

There was a lot of hassle earlier this year regarding certain government documents, which may or may not have been confidential, or had been forgotten, that were used in the coalition-formation talks. In the end it turned out that RSM research was used as evidence for abolishing the dividend withholding tax. What is your opinion of the role of academic research in the process?

“Based on that RSM study it’s simply impossible to conclude that the dividend withholding tax should be abolished. The report isn’t even about that. Corporate executives were interviewed about crucial location factors to establish their company in the Netherlands. The term ‘dividend withholding tax’ only appears twice, in parentheses. The decision-making process is a textbook case of reverse engineering: there was already a policy proposal, and politicians and policy makers then tried to collect some evidence to support it. However, there was not a shred of serious research available, so they resorted to the RSM-report instead. This obviously has nothing to do with evidence-based policy making.”

It seems that over the past few decades, it has become a goal in itself for the Netherlands to attract and retain companies. Is abolishing the dividend withholding tax a part of a wider trend?

“Definitely. We have a bad reputation when it comes to dealing with tax avoidance. We are regularly admonished by the European Commission for harmful tax practices. A good example of this is the ‘ruling practice’ where corporations can make special tax agreements with the tax authorities. Moreover, due to loopholes in the network of tax treaties and not levying taxes on royalties, companies like Google, Facebook, Microsoft and Apple were able to channel their profits to tax havens via the Netherlands.

“There are only a few countries in Europe that don’t have a dividend withholding tax: the United Kingdom, Estonia, Latvia and Hungary. Other countries are tax havens such as the Cayman Islands, Bahrain, Liechtenstein, Malta and Bermuda. Now the Netherlands joins this club of countries.

“Governments are engaged in a in a race to the bottom in their attempts to improve the business climate. The Netherlands has been acting aggressively. Whether it’s about international tax legislation or combatting climate change, this is a classic prisoner’s dilemma. Seen from an international competition perspective, one can understand that the Netherlands refuses to introduce CO2 pricing or to raise taxes on multinational companies. But if everyone does the same, we will end up in a world with catastrophic climate change and where footloose multinational companies barely pay any corporate taxes. The tax burden then necessarily shifts from capital to labour, from shareholders to workers. That will increase income inequality.”

Image by: Bas van der Schot

‘The Netherlands will become even more prominent in rerouting corporate profits to tax havens’

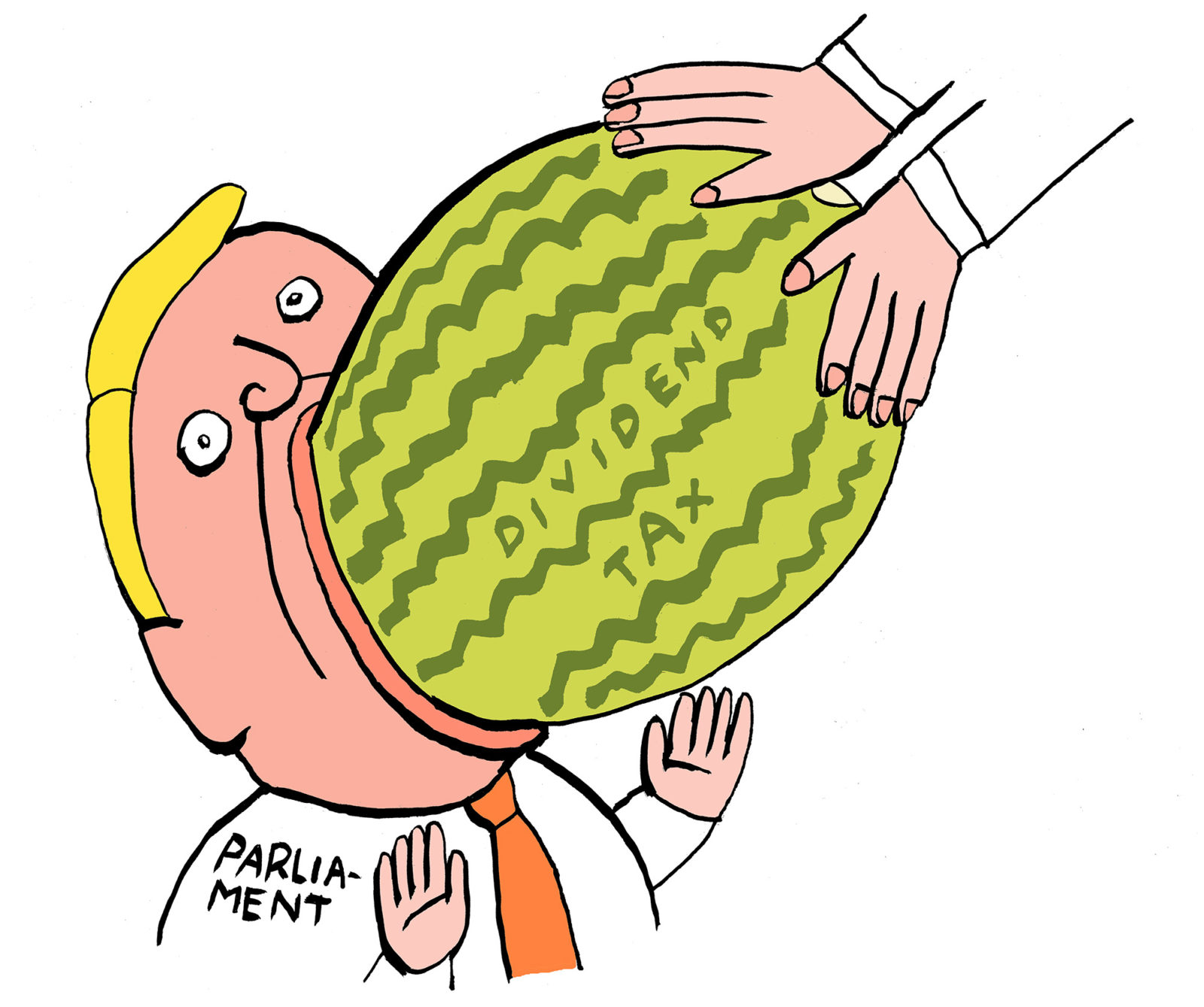

Abolishing the dividend tax will cost 1.9 billion euros, half a billion more than initially estimated. The measure will now be financed by reducing the corporation tax by a lower amount than originally proposed (from 25 to 22 percent instead of 21 percent). So firms share in the costs. That seems fair, doesn’t it?

“It seems fair at first glance, but from an economics point of view it’s a bizarre choice. The corporate income tax has many more drawbacks than the withholding tax on dividends. The dividend withholding tax is an implicit tax on other governments, while the corporate tax has a direct impact on four important decisions companies make, as academic research has clearly demonstrated. How much do firms invest? To what extent they finance these investments with debt – where interest costs are deductible – or with equity – where dividend payouts are not deductible? Where will they locate? And how much do they avoid taxes by shifting profits around? If there is one tax cut that can be justified by academic research it is lowering the corporate income tax.”

Suppose the measure to abolish the dividend tax passes the Upper House later this year, would this have an impact of the credibility of the Netherlands?

“Based on the analyses of the Netherlands Bureau for Economic Policy Analysis (CPB), I think that the Netherlands will become even more prominent in rerouting corporate profits to tax havens. This damages our international reputation. But what’s even more important is that it is not in the general interest of the Netherlands to do this. We are spending 2 billion euros per year despite that there is no solid evidence that suggests that this measure is necessary.”

De redactie

Latest news

-

Agreements on international students now officially formalised

Gepubliceerd op:-

Education

-

Internationalisation

-

-

Looking for Woudestein’s wildlife with nature expert Jacob Molenaar

Gepubliceerd op:Article type: Video-

EM TV

-

-

Student union starts petition against increase in tuition fees for international students

Gepubliceerd op:-

Money

-

Comments

Comments are closed.

Read more in The Issue

-

‘Most medical influencers do not think they are unqualified’

Gepubliceerd op:-

The Issue

-

-

War in Iran: will the energy transition get a push or a blow?

Gepubliceerd op:-

The Issue

-

-

How expensive festival tickets and major concerts are threatening the entire live music sector

Gepubliceerd op:-

The Issue

-