‘Central Bank needs to accelerate energy transition’

The European Central Bank’s monetary policy should contribute to the EU’s climate targets, says Finance professor Dirk Schoenmaker. “The stimulus package currently undermines sustainability and indirectly favours companies in the fossil fuel sector.”

Image by: Bas van der Schot

Dirk Schoenmaker is Professor of Banking and Finance at Rotterdam School of Management. His research focuses on monetary policy, the role of central banks, financial stability, and European financial integration. He recently presented the paper Greening Monetary Policy(2018) to the CPB Netherlands Bureau for Economic Policy Analysis, and he is the author of the newly published book Principles of Sustainable Finance.

Over the past few years, the European Central Bank (ECB) has purchased corporate bonds worth 178 billion euro within the 2,500 billion euro buying programme. This includes many companies responsible for pollution. You recently published a paperin which you proposed that the European Central Bank’s monetary policy should benefit sustainable sectors more and favour polluting sectors less. Why?

“The primary purpose of the central bank is to work towards price stability within the entire European economy. Nothing more, mothing less. If the economy overheats, you raise interest rates to reduce the chance of inflation. If you want to stimulate the economy, you reduce interest rates. To that end, the ECB issues loans and buys bonds. It does this in all sectors, without discrimination. As a result, a company such as Ahold, either through a bank or by other means, can obtain funds under the same terms as Shell. In policy terminology, we refer to this as market neutrality. But the problem as I see it is that the incentive policy isn’t as neutral as it’s made out to be. The reason for this is carbon bias. Companies with high CO2 emissions turn out to be more capital-intensive, and therefore they benefit much more from the ECB’s stimulus measures.”

So polluting companies are currently being favoured?

“Yes. A car manufacturer needs much more money than a consultant. So the car manufacturing sector issues more bonds and benefits more across the board from specific ECB stimulus measures. That makes the monetary policy incompatible with European Union policy, which in fact aims to reduce emissions. That makes for a strange situation.”

What are you proposing?

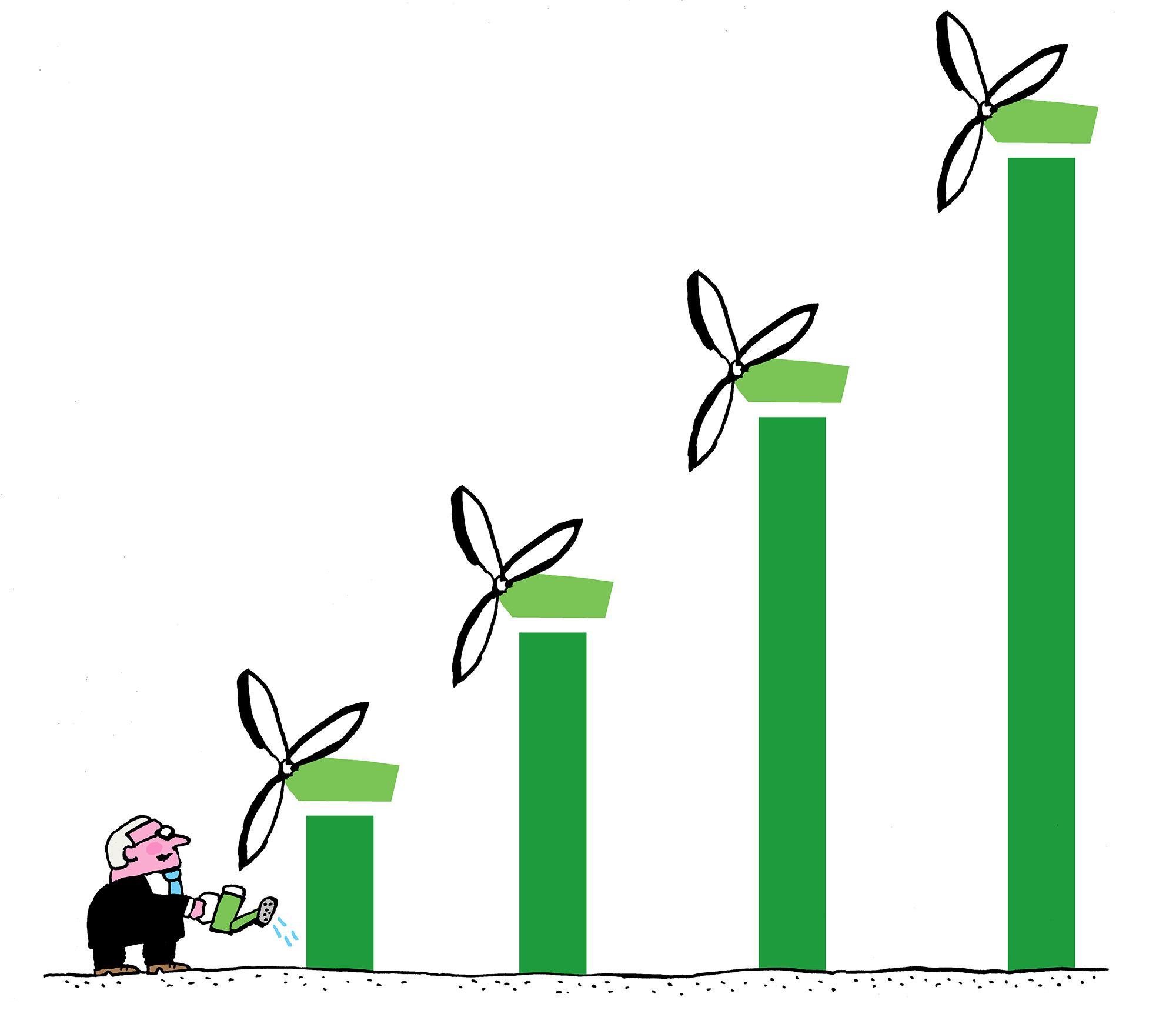

“The ECB’s stimulus package now puts sustainable companies at a disadvantage. In my opinion it should work to their advantage. You could do this by dividing the market into three categories: low carbon emissions, medium carbon emissions, and high carbon emissions. And you would no longer buy equal amounts of instruments across the board. Instead, you would reduce what is bought from the high emissions category by half. Instruments bought from the medium emissions category would be reduced by a quarter, and you would then buy three-quarters more from the low emissions category. This way you still serve the entire economy, but the capital costs of companies with low CO2 emissions are reduced. This way, the capital market induces reforms.”

‘The problem as I see it is that the incentive policy isn’t as neutral as it’s made out to be. Companies with high CO2 emissions turn out to be more capital-intensive, and therefore they benefit much more from the ECB’s stimulus measures’

Image by: Bas van der Schot

How do you know that will actually occur?

“It has been calculated that a shift would take place if more than twenty percent of financiers would switch from fossil fuel companies to green companies. That would lead to such an interest rate change that it could be an incentive to, for example, start using low carbon production methods. Investors – and this includes a central bank – could help companies make this switch.”

According to critics, the ECB would be venturing into the political arena if it did that. Your fellow economist and former deputy director of CPB Netherlands Bureau for Economic Policy Analysis Clemens Kool stated in NRC that you would be making an appeal for ‘activist policy’.

“That’s an important point. The independence of central banks is a significant asset. Scientific research has shown us that an independent central bank is better for price stability than a politically driven one. If you allow political interference in central banks, they’ll start handing out favours whenever elections are around the corner. The Bank of England was political in the past and that resulted in much higher inflation expectations. You shouldn’t be pursuing your own policy as a central bank. But in addition to their primary purpose, central banks also have a legal mandate to support EU policy. And that is not without reason. And it’s happening as we speak. The current stimulus policy – which is not undisputed – is in place to stimulate economic growth. That is not the primary purpose of the ECB. Look, if there were a contradiction between price stability and stimulating sustainability, then you should avoid it. But I don’t see any contradiction. And if it involves such an important EU priority, then I say: at the very least, the ECB shouldn’t hinder sustainability.”

In Europe we also feel that issues such as combating poverty or attaining equality between men and women are also important. Today the issue is climate change, tomorrow it’s gender equality. Where do we draw the line?

“There is no other issue that enjoys such widespread consensus. Climate policy has been a top priority for the European Council and the European Commission for ten years now. For the past two years, the European Parliament has been asking ECB President Mario Draghi why he hasn’t taken action.”

‘If we end fossil fuels today, no vehicles will be running tomorrow. That would be disastrous for the economy.’

Klaas Knot, President of De Nederlandsche Bank (DNB, Central Bank of the Netherlands), recently advocated a CO2 tax when he appeared on the Buitenhof television programme. In October, he particularly urged the government to not delay taking action to tackle climate change. Further delay would result in a greater chance that ‘abrupt’ measures would be needed later, which could lead to ‘heavy losses’ in the financial sector. To what extent do low CO2 emissions ultimately benefit price stability?

“This wasn’t the principal argument in my paper, because this is difficult to prove. But it’s plausible that a steady transition towards a more sustainable economy could prevent shocks to price levels and thus prevent unnecessary damage to the economy. And a central bank could certainly lend a helping hand here.”

You propose a small shift from high-emission companies to low-emission companies. Wouldn’t it be a good idea to cut off funds altogether for polluting companies?

“The percentages I proposed are a shot across the bow. It’s an informed attempt to steer the discussion. But it’s entirely possible that these figures may have to be revised. However, I don’t believe that excluding CO2-intensive companies would work. The process needs to be a transition from point A to point B. If we end fossil fuels today, no vehicles will be running tomorrow. That would be disastrous for the economy.”

Image by: Bas van der Schot

The ECB has announced that it is ending the incentive programme. Is your analysis still relevant?

“My story is still relevant even when no new bonds are being bought. That’s because collateral has been provided for the outstanding portfolio. In the conditions for acceptance for the collateral, the ECB can be stricter when dealing with high-emission companies.”

You sketch a picture of an orderly world where it’s easy to determine emission levels relative to loans. But the financial sector has become more complex over the past decades. The last crisis was partially the result of financial products that were so fragmented and intermixed that it became practically impossible to make a credit risk assessment. Is it possible to do that for CO2?

“Yes. In the near future it will be mandatory for companies to publish their carbon emission intensity. That’s a reliable indicator that can be used for this purpose.”

Is this shift going to happen?

“Right now, central banks find it a scary proposition, but these things take time. Ten years ago people thought it was perfectly normal for pension funds to invest in the fossil fuel industry, or even in the arms trade. It didn’t matter as long as it yielded maximum returns. Now people have come to realise that sustainable investment can achieve the same results. It’s gotten to the point where you have to explain why you’re not making sustainable investments.”

De redactie

Latest news

-

Agreements on international students now officially formalised

Gepubliceerd op:-

Education

-

Internationalisation

-

-

Looking for Woudestein’s wildlife with nature expert Jacob Molenaar

Gepubliceerd op:Article type: Video-

EM TV

-

-

Student union starts petition against increase in tuition fees for international students

Gepubliceerd op:-

Money

-

Comments

Comments are closed.

Read more in The Issue

-

‘Most medical influencers do not think they are unqualified’

Gepubliceerd op:-

The Issue

-

-

War in Iran: will the energy transition get a push or a blow?

Gepubliceerd op:-

The Issue

-

-

How expensive festival tickets and major concerts are threatening the entire live music sector

Gepubliceerd op:-

The Issue

-