Students’ housekeeping books reasonably well balanced

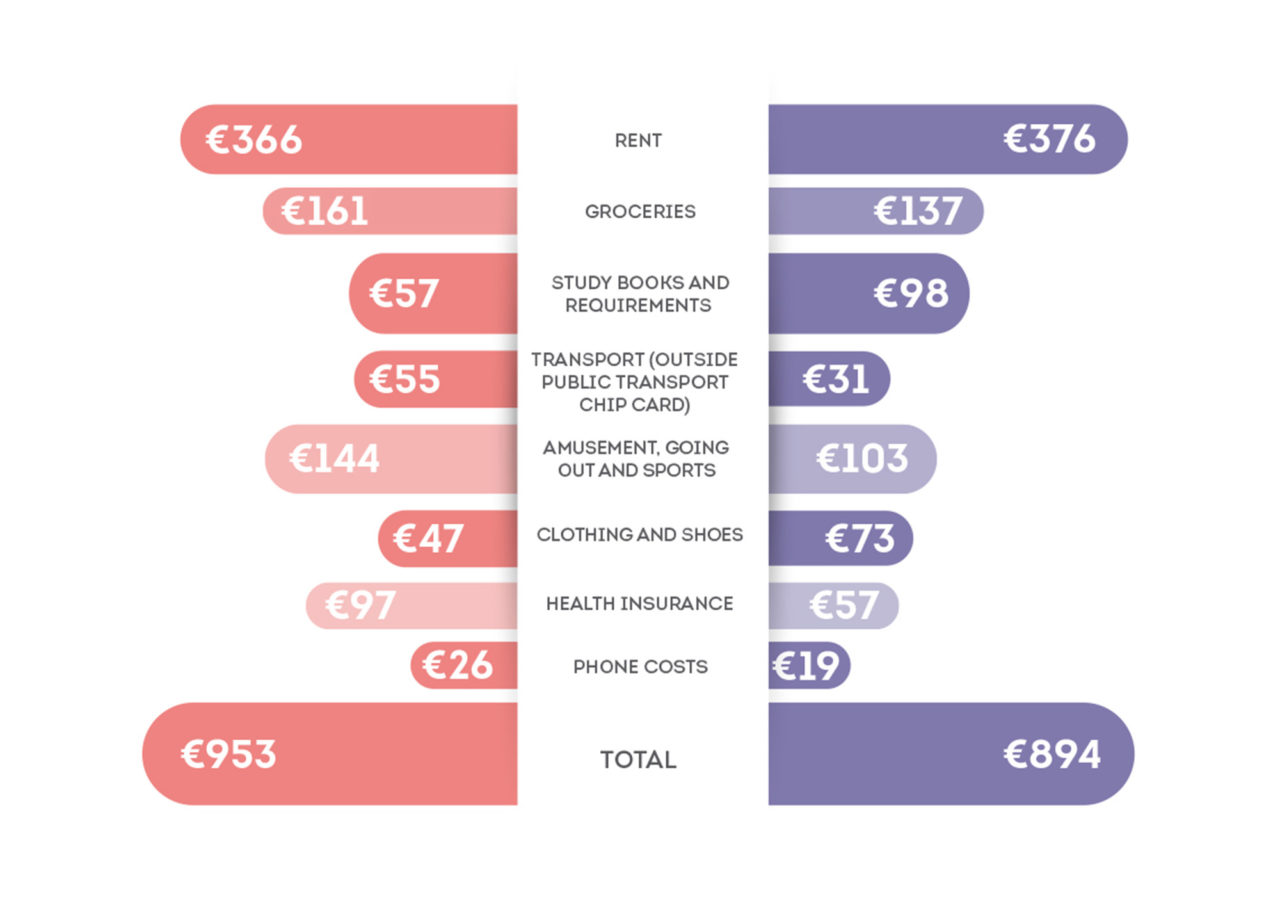

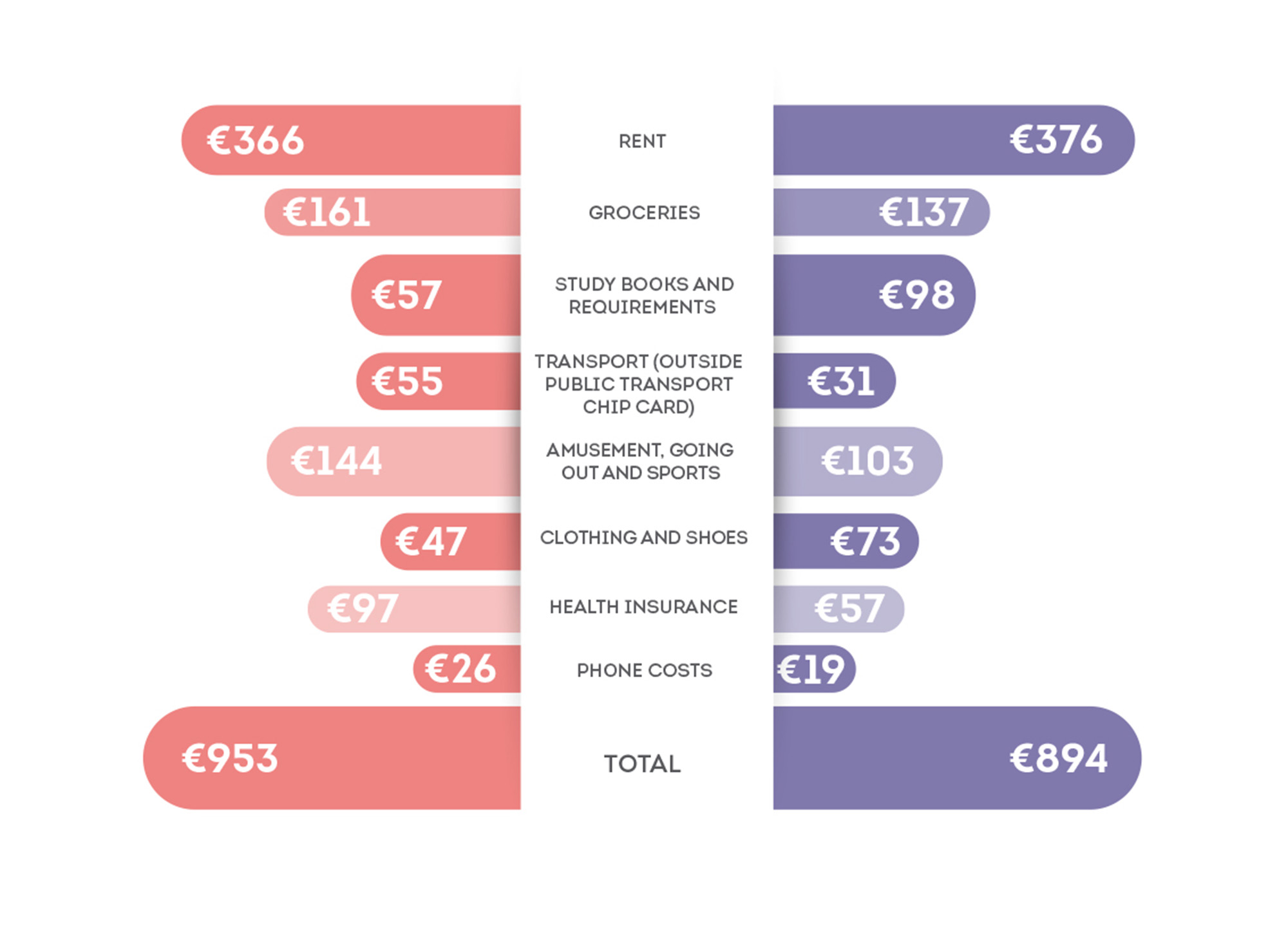

Monthly costs for students who live away from home, according to Nibud (left) and the guess by first-year students of the Erasmus University Rotterdam (right)

Image by: Unit20

Room rent rates and tuition fees are rising, standard student grants have been abolished and students are increasingly being forced to borrow money. Even so, they generally manage to stay on top of their finances, an EM survey shows.

Students are greatest victim of purchasing power decrease in 2017.” This was students’ interest group ISO’s headline at the end of August. According to ISO’s purchasing power calculations, students will be hit the hardest, partially due to rising tuition fees and the abolition of the standard student grant. Given these circumstances, EM‘s editors found themselves wondering – do first-year students know what they are getting into, and have they made sufficient financial arrangements to keep their heads above water? In order to help us find out, 138 students completed a survey on their situation and their expectations.

Monthly costs for students who live away from home, according to Nibud (left) and the guess by first-year students of the Erasmus University Rotterdam (right)

Image by: Unit20

Let’s start with a reassurance. Generally speaking, students have a pretty good idea of the costs associated with being a student, although they tend to be just a little too optimistic. For instance, students expect their monthly public transport expenses which are not covered by their public transport chip cards to amount to €31, although the National Institute for Family Finance Information (Nibud) puts the figure at €55 per month.

A further discrepancy between wishful thinking (the amount first-year students believe they will spend each month) and reality (the monthly average calculated by Nibud) can be observed in the money students expect to spend on health insurance premiums. Nibud believes the monthly average to be €97, whereas the students expect only €57.

Image by: Sanne van der Most

Eva Lange (17, first-year Law)

“I’m currently borrowing money from DUO. Some of this will later be repaid by my parents, as this proved to be the cheapest solution at the current interest rate. Of course, I will have run up quite a debt by the time I graduate, but I mainly regard that as a solid investment. I will pay off my debt once I get a job. I still live with my parents, which is obviously much cheaper. However, I’m also doing it because I want to check in this first year whether I actually like my degree course. If so, I definitely intend to move out next year, which will obviously cost more. In order to earn a bit on the side, I work at a tapas restaurant. I’m not earning a lot of money, but I’m having a great time! I spend most of my money on holidays, clothes and my studies. Other than that, I don’t spend too much. If I were ever to run out of money, I’d cut down on clothes first. I generally buy sensibly, but every now and then I’ll buy something I don’t need at all, such as an extra pair of trousers. In addition, I’m saving for my tuition fees and for the room I’ll start renting next year. I think it’s only sensible to plan ahead.”

Conversely, students believe certain expenses to be greater than Nibud’s calculations would seem to indicate. For instance, students expect to pay an average monthly rent of €376, even though Nibud puts the figure at €366. Furthermore, they believe to spend €98 per month on textbooks and other things they require for their studies, although Nibud claims €57 per month is more likely. The same thing is true for clothes and shoes: students count on a monthly expense of €73, whereas Nibud puts the number at €47. According to Nibud spokesperson Annemarie Koop, many students believe that they have their finances straighter than their peers who do not attend university. “But they know less about insurance policies. They don’t know exactly what concepts such as deductibles, premiums and terms and conditions mean.”

Overestimated expenses

Parents who are having difficulty letting their children move into the world will be comforted by the knowledge that their kids have a pretty good idea of their expected expenses. Clearly, these parents do not allow their children to move out without giving them some small measure of preparation. For instance, a very significant majority of parents indicated that they had prepared their children for living independently, according to a study conducted this summer by the “Wijzer in geldzaken” (More Sensible with Money) Platform, which was established by the Ministry of Financial Affairs. The study surveyed parents whose children are about to move out or are planning to do so in order to attend uni. The study showed that three out of five parents had sat their children down in order to identify expected income and expenses with them.

Image by: Sanne van der Most

Pim Spaanjaars (18, first-year Econometrics)

“I live with two other people in an apartment in Capelle, which costs me 450 euros per month. I’m borrowing the maximum amount of one thousand euros per month from DUO. From now on, that will be deposited into my bank account each month. Because I’ve only just turned eighteen, I won’t receive any money for the first few months, which kind of sucks. I think that amount will be more than enough for me to make ends meet, although nearly half of it will obviously go towards my rent. Of course, my expenses will occasionally exceed my loan. For that reason, I definitely intend to get a side job, such as maths and physics tutoring. My parents have told me that as long as things continue to go well, they will not pay any of my expenses. They feel it’s my own responsibility, and that I must make my own arrangements. However, should I really get into difficulty, they will help me out. That’s a reassuring thought. Once I complete my degree, I will obviously have a fairly significant debt of some 48 thousand euros, plus interest. That’s not great, but that’s life. Thankfully, econometrics graduates have pretty decent job prospects, so I’m not too worried.”

For its part, EM’s survey also showed that parents are actively involved in their children’s finances. Ninety-two students reported discussing their finances with their parents. One hundred and seven students said they receive financial support from their parents, the average monthly contribution being €529. This includes payments towards the students’ tuition fees, health insurance premiums, textbooks and rent.

Financial tips

Percentage of parents that give financial support to their children, according to national Nibud research (left) and research by EM among first-year students at Erasmus University (right).

Image by: Unit20

According to ISO’s purchasing power calculations, it is mainly rent rates and tuition fees which are straining students’ budgets, since both go up each year. The Minister of Education has admitted as much, but is of the opinion that students must simply take out bigger loans. “So basically, you’re saddling students with debts that will be huge by the time they graduate,” said ISO President Jan Sinnige. “Surely that can’t be a solution?”

Therefore, ISO hopes that Minister of Education Jet Bussemaker will unveil new measures to make things easier for students on the day of the King’s annual speech (20 September). “For instance, ensure that tuition fees don’t go up after students embark on their degrees, so that they know what they will be expected to pay down the track,” Sinnige advocates.

Image by: Sanne van der Most

Houda Boulakhrif (18, first-year business administration student)

“My parents live in Rotterdam and I’m enjoying living with them. Why spend a lot of money on an expensive room when I can live comfortably at home? Especially during my first year. I will take out a student loan in the future. Not that my parents can’t afford to pay my fees, because they’re also paying for my clothes. I must pay my tuition fees and my textbooks myself, though. Fortunately, they have saved money for me all my life, which will see me through my first year at the very least. It’s a nice buffer. As for what happens after that, I’ll cross that bridge when I find it. My parents taught me well how to deal with money. I was given some money of my own at a fairly young age, which gave me reasonably sensible spending habits. They taught me that if I really want to have something, I must save money for it and prioritise, which may involve refraining from doing certain things. But they also taught me that it’s sometimes good to pay a little extra for high-quality products. I spend most of my money on going out for dinner or drinks. Every day, I’ll bring home-made sandwiches with me, only to pop into SPAR to get myself a nice bun. Perhaps that’s not the smartest thing to do, but I do love it!”

And what about those students who have just embarked on their degrees? What would Sinnige advise them to do? “Make sure that you take a good look at all the plans offered by DUO, at the very least. For instance, apply for a supplementary grant, even if you think you’- re not eligible for one. For you may not be eligible at present, but terms and conditions do change,” ISO’s President suggested. “Also take a look at the extra allowances you may be eligible for. To do so, check out the websites hosted by the government, the municipal authorities and the universities.”

Get your expenses straight

EM’s study showed that if EUR students should fall on hard times financially, nearly half of respondents intend to spend less money on clothes and going out. In addition, they intend to resolve potential or actual overdrafts by getting a job, working more hours, or borrowing more money. Twenty-nine respondents indicated that they expected the former strategy to prevent them from incurring debts. Students who have a student loan expect to owe on average well over €20,000 after obtaining their degrees.

“At least once in your time at uni, draw up a financial overview. Not only will it help you get a better understanding of what you are spending each month, but it will tell you what income is missing.”

Annemarie Koop, spokesperson Nibud

Annemarie Koop, spokesperson Nibud

In closing, Nibud spokesperson Annemarie Koop provided one more tip on how to limit the damage. “At least once in your time at uni, draw up a financial overview. Not only will it help you get a better understanding of what you are spending each month, but it will tell you what income is missing. For instance, many students forget to apply for a health insurance allowance, even though the application process is very straightforward.” She also recommends checking all your bank statements once in a while to get an idea of what withdrawals are being made. “If you do that, you may find that you are still paying membership fees for a club in your parents’ village, even though you haven’t attended a club event for years. Going through all these individual withdrawals will really help you make useful decisions. If you’re still short on cash, it will help you determine what to cut down on.”

Latest news

-

Wooden ‘Berlin wall’ hides exterior of Exam Centre

Gepubliceerd op:-

Campus

-

-

Agreements on international students now officially formalised

Gepubliceerd op:-

Education

-

Internationalisation

-

-

Looking for Woudestein’s wildlife with nature expert Jacob Molenaar

Gepubliceerd op:Article type: Video-

EM TV

-

Comments

Comments are closed.

Read more in Student life

-

Marcroix celebrates its 100th anniversary: ‘Are you ready for a little gallop?’

Gepubliceerd op:-

Student life

-

-

The impact of AI on entry-level jobs: no reason to panic, but much to think about

Gepubliceerd op:-

Artificial Intelligence

-

Student life

-

-

World Cup participation means a lot for Curaçaoan students: ‘For the first time you see your country being recognised’

Gepubliceerd op:-

Student life

-